How Much Does It Cost to Remove Debt Review in South Africa?

If you've paid off your debt or regained financial control but you're still blacklisted under debt review, you're not alone. Many South Africans remain flagged even though they no longer need protection. This “credit bureau adverse listing flag” holds them back from buying a car, getting a home loan, or even opening a store account.

At Credit Salvage, we specialise in legally removing that flag through proper channels using court applications, credit bureau engagement, and post-removal aftercare.

This article breaks down the real costs, explains the removal process, and answers common questions so you can take back control.

What Is Debt Review Removal?

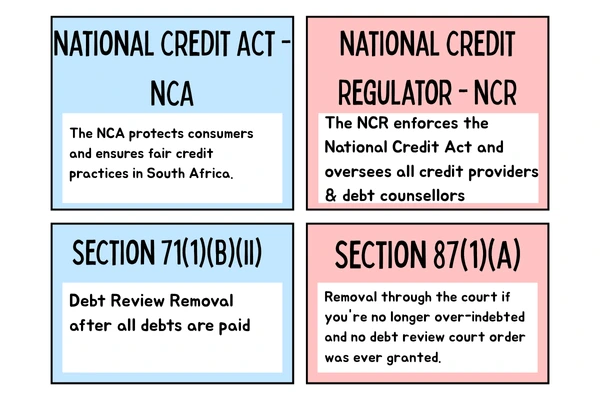

The removal process is the legal process of clearing the “under debt restructuring” status from your credit profile. This flag was placed to protect you but once you’re no longer over-indebted, or your debts are settled, it becomes a barrier.

At Credit Salvage, we follow National Credit Act (NCA) rules to ensure you're cleared:

With a Form 19 certificate (if all debts are paid), or

Through a magistrate’s court order (if a court order exists or your debt counsellor won’t cooperate)

How Much Does It Cost to Remove Debt Review?

Here’s what you can expect to pay:

| Your Situation | Removal Route | Estimated Cost |

|---|---|---|

| All debts settled | Form 19 Clearance Certificate | R3306 |

| No restructuring court order and Debts not fully paid. | Court reassessment | R8118 |

What You’re Paying For

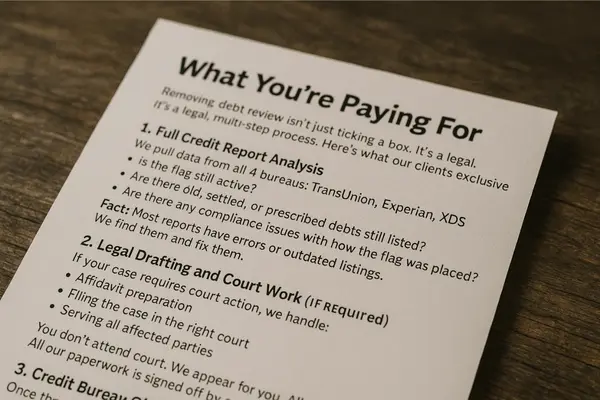

Removing this credit bureau indicator isn’t just ticking a box. It’s a legal, multi-step process. Here's what our clients exclusively get:

1. Full Credit Report Analysis

We pull data from all 4 bureaus: TransUnion, Experian, XDS, and Compuscan. We check:

Is the flag still active?

Are there old, settled, or prescribed debts still listed?

Are there any compliance issues with how the flag was placed?

Fact: Most reports have errors or outdated listings. We find them and fix them.

2. Legal Drafting and Court Work

If your case requires court action, we handle:

Affidavit preparation

Filing the case in the right court

Serving all affected parties

You don’t attend court. We appear for you. All our paperwork is signed off by registered attorneys.

3. Credit Bureau Clearance

Once the certificate or court order is granted, we submit it to all 4 major bureaus, THE NCR and your crediotrs and follow up until:

The credit bureau indicator for debt restructuring is fully removed on ALL the above databases

Your profile reflects “cleared” status

Important: If even one bureau doesn't update your status, your loan applications, homeloans, vehicle finance applications and even job applications will still be rejected. We ensure complete clearance.

4. NCR Engagement

If a court order declaring you no longer overinded, we also notify the National Credit Regulator with the supporting documents ensuring there’s no future dispute or “re-flagging.”

5. Free 6-Month Aftercare

Once you're cleared, we continue to support you:

Help rebuild your credit score

Guide you through new credit applications

Deal with and/ or dispute any leftover adverse, or unfair listings

Advice: Registered Credit Providers look for a 12-month clean payment history post the debt counselling process. We’ll help you get there - FOR FREE

Apply online here to start the removal process

Why Choose Credit Salvage?

| Feature | Credit Salvage | Many Other Providers |

|---|---|---|

| Court-based legal removal process if no court order exist | ✅ | ❌ |

| Handles all 4 bureaus | ✅ | ❌ |

| NCR escalation with court order (if needed) | ✅ | ❌ Only issues clearance certificates |

| Flat-rate pricing with the option to repay in monthly installments | ✅ | ❌ |

| 6-month aftercare | ✅ | ❌ |

| No empty promises | ✅ | ❌ |

Why Wait? Credit Salvage Is South Africa’s Trusted Name in Credit Bureau Removals

At Credit Salvage, we don’t just delete credit bureau indicators for debt restructuring indicators we restore your financial freedom. With over 500 verified positive 5 star reviews, we are known for delivering real results that last. Our legal team handles the full process from court application to bureau clearance, and our pricing is honest: no hidden fees, with flexible repayment options that work for your budget.

When you choose us, you get more than a service. You get:

A dedicated legal team

Complete credit report audits

Full credit clearance across all four major credit bureaus

6 months of free aftercare to help you rebuild and recover

But here’s the truth: the longer you wait, the worse your situation becomes.

Every month under debt counselling keeps your credit score frozen.

You miss out on housing, car finance, and even job opportunities.

Your credit bureau indicator continues to scare off credit providers no matter how much you are earning now.

The court process does not start until you do. And some listings may eventually expire or prescribe, but others will linger for years unless removed through a legal process.

Waiting does not fix the problem. Action does. Start today and take the first step toward a clean, credit score ready profile. With Credit Salvage, you're not just another case number you are a real person, and we fight to clear your name.

“Credit Salvage didn’t just clear my name they helped me rebuild my credit score step by step.” Thandi M., Cape Town

How Long Does It Take?

Clearance Certificate (Form 19): 2–3 weeks

Court application route: 4–8 weeks (depends on court schedule and your documentation)

We give you a timeline upfront and we stick to it.

Apply online here to start the removal process

Can You Do It Yourself?

Short answer: No. The bureaus won’t accept removal requests without the following documents. You need:

A clearance certificate (Form) 19 from a debt counsellor, or

A court order declaring you're no longer over-indebted

Credit Salvage handles both routes legally, quickly, and without confusion.

Frequently Asked Questions (FAQs)

How Can I Remove unpaid Debt from My Credit Record?

By settling it, disputing incorrect listings, or proving it's prescribed or unlawfully listed. We identify and help remove all valid negative listings legally.

How Long Does It Take to Remove the Debt Review Flag?

2–3 weeks (Form 19 route) or 4–8 weeks (court route). We handle all the paperwork and push for fast results.

How Do I Get a Clearance Certificate After Debt Counselling?

Once you’ve paid off all listed debts,we issue a Form 19.

What’s the Fastest Way to Get Out of this process?

Pay all listed debts or prove you’re no longer over-indebted. We handle the legal process to exit you properly.

Can I Get a Loan While Under Debt Review?

No. It's illegal for credit providers to offer you any credit facilities until the credit bureau indicator is removed. We’ll help you clear it so you can apply again.

Can the NCR Remove Me from Debt Review?

No. Only your a counsellor or a court can remove you. We handle the full court process if needed.

How Much Does It Cost to rescind Debt Review?

Between R3306 and R8118 depending on your case. We offer fixed fees and affordable monthly repayment options.

Can a Lawyer Remove Me from Debt Counselling?

Yes, and that’s exactly what we do. Our legal team handles court drafting, filing, and removal.

How Do I Get My Debt Cancelled?

Some debt can be cancelled if it’s prescribed (older than 3 years, no payments or acknowledgements). We investigate each listing for you.

Will My Debt Review Flag Be Removed Automatically?

No. It stays there until it’s removed via Form 19 or a court order. We make sure it’s gone legally and for good.

Is Debt Counselling a Criminal Record?

No, but it still prevents you from getting credit or if you work in the finance industry you might not even quaify for a new position. We remove it legally and help restore your status.

Who Is Credit Salvage?

We are a registered debt counselling and credit restoration firm helping all South Africans:

Remove the debt counselling flag

Clean their credit reports and assist with credit score increases

Rebuild their financial lives

We work with integrity, transparency, and results.

Apply online here to start the removal process

Ready to Clear your credit bureau profile and increase credit scores?

Call: 0878980895

Email:

Visit: www.creditsalvage.co.za

- Start with a free assessment.

- Pay only if you qualify.

- Let us handle everything from court to credit clearance.

Apply easy online here Credit bureau removal application

"Fix your name. Reclaim your future." – Credit Salvage

Case Study: Debt Review Removal for a Married Couple – One Price, Two Lives Changed

Background

Sipho and Lerato M, a married couple living in Pretoria, were placed under debt counselling in 2019 after facing financial strain due to job loss and medical expenses. Soon after Joining debt counselling they advised their debt counsellor they will be paying their accounts on their own and they istructed the debt counsellor not to proceed with the debt restructuring court order. Married in community of property, all their debts were legally shared and managed together under a joint debt restructuring application under debt counselling.

Over time, their situation improved:

Sipho found permanent employment

Lerato’s side business grew steadily

Together, they managed to settle most of the accounts listed

But there was a problem. Despite settling most of their debts, their credit reports still showed them under debt restructuring, blocking access to:

Home finance for their growing family

A small business loan for Lerato’s company

A vehicle upgrade, despite a solid joint income

Frustrated and misled by other companies charging separate fees for each spouse, they turned to us for help.

Our Solution: Joint Debt Review Removal, One Price, Two Results

We understood immediately that their financial histories were legally tied together. Instead of treating them as two separate cases, we processed them as one legal unit under a single court application as there was no debt restructuring court order in place.

Here’s what we did:

Step 1: Free Joint Assessment

We reviewed both credit reports, confirmed that most debt obligations were paid in full, and verified there were no outstanding judgments or defaults holding them back.

Step 2: Legal Drafting & Court Application

Our legal team:

Drafted a joint affidavit declaring they were no longer over-indebted

Filed one combined court application for debt restructuring removal

Appeared in court on their behalf (no attendance required)

Step 3: Bureau Clearance

Once the magistrate granted the order, we submitted it to:

- The NCR. The NCR updated their status code effectively removing the debt restructuring listing

TransUnion

Experian

XDS

Compuscan

We followed up until both Sipho and Lerato’s profiles were cleared.

Extra Value Provided by Credit Salvage

One flat fee for the couple, no double charges

Interest-free payment option to suit their cash flow

6 months of free aftercare: We helped Lerato apply for a business account and monitored Sipho’s credit score to prepare for a home loan

Prescribed debt screening: we flagged and removed 2 older listings that had long expired but were still listed on their profiles

Client Testimonial

“We thought we had to pay twice. Credit Salvage treated us as a family not a sales number. They explained the law, kept us updated, and within weeks, we were finally free. We bought a car. We applied for credit cards. We feel like adults again.”

— Sipho & Lerato M, Pretoria

The Outcome

The Debt counselling indicator removed for both husband and wife

Full clearance on all bureaus

New vehicle financed within 3 weeks

Business account approved for Lerato’s growing venture

Improved credit scores and zero negative listings

Key Takeaways

Benefit Result Joint removal process One court case handled both spouses Flat-rate pricing Affordable and transparent Legal route Fully compliant with the National Credit Act Full bureau follow-up No partial removals or loose ends 6-month support Ongoing credit monitoring and guidance

Are You a Married Couple Under Debt counselling/ restructuring?

If you're married in community of property, you don’t have to go through two separate processes. Credit Salvage helps couples exit this process together, legally, affordably, and for good.

We clear both your names for one price. Let us help you take back your financial freedom.

Apply here for debt review removal

Related Articles:

How Much Does It Cost to Remove Debt Review

How Credit Salvage Helps You Remove the Debt Review Flag

Boosting Your Credit Score After Debt Review

What to Do When You Receive a Demand Letter